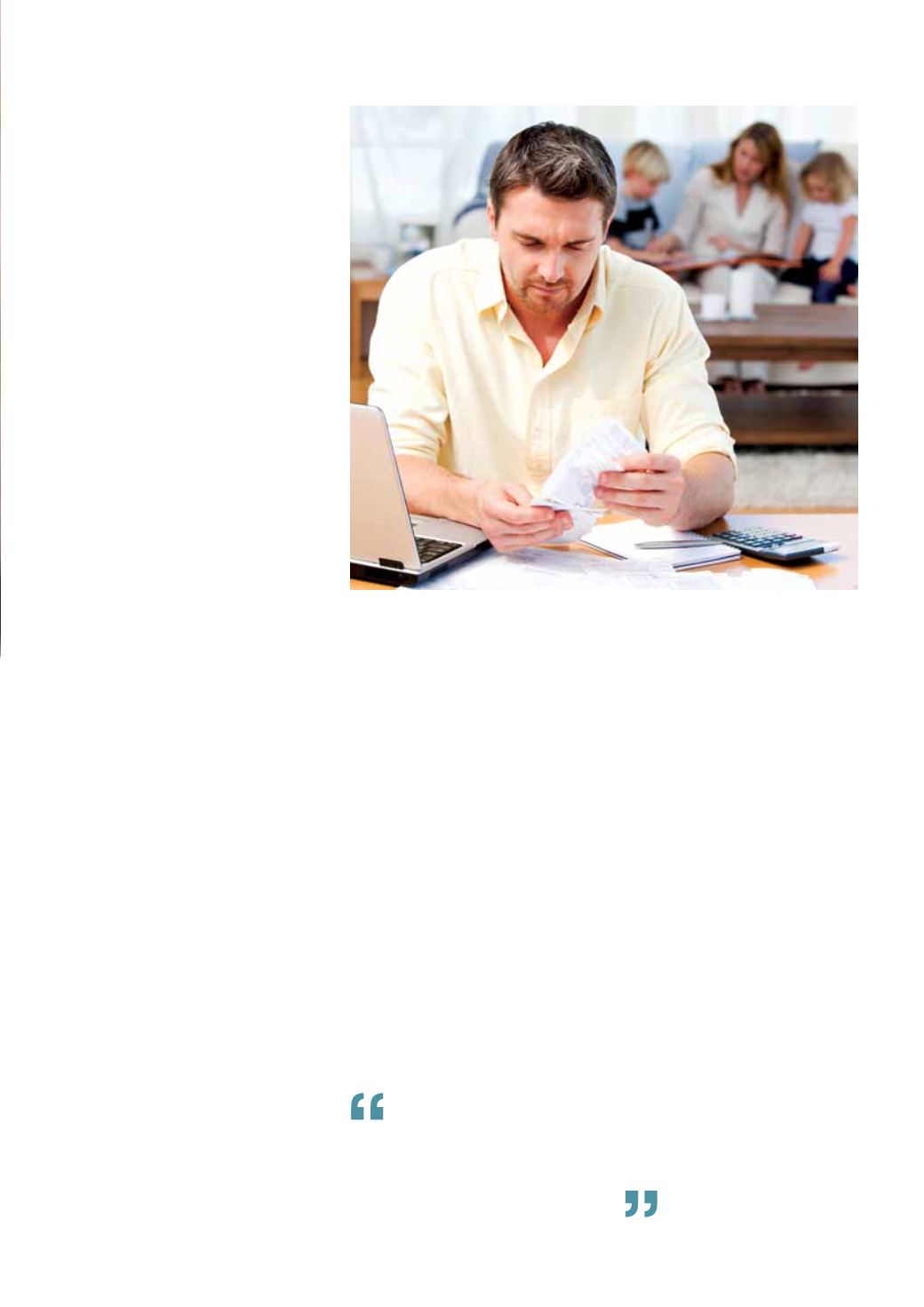

wish. “If what we spent on the kids

last month seemed high, we can just

go into the category on the computer

and see where the money went,” says

Samantha Harvey Saxena, who uses a

budget tracker app called Koku.

Samantha decided to implement

a budget about a year ago to monitor

spending. “Initially it was an exercise

to see just how much we were

spending, because we had no idea,”

she says.

Her financial reports revealed a

few surprises – like the extra $1,000

spent at duty-free while travelling.

Another discovery confirmed

suspicions on how much money

was spent on the children, between

school fees, “which we can’t do much

about,” to unnoticed medical costs, to

extracurricular activities and treats.

“A hundred dollars here and there

with two kids becomes a lot very

quickly,” says Samantha.

The tracking has helped them

tailor their spending in a number of

ways. Samantha says she discovered

vaccines were cheaper at private

hospitals than at a nearby practice.

She also fixed a sum for discretionary

spending on the children, easing her

mind quite unexpectedly. “If you have

a budget that you’ve decided is more

than enough, you avoid feeling guilty

saying no when they ask for more,”

she says.

Fixing the magic number

To implement a change in spending

habits, identify monetary goals with

your partner. Planning for children’s

education is high on many priority

lists, as is setting up financial security

for old age. But factor in the fun stuff

too, like how many holidays you want

to take each year. Work towards

compromise on both sides of the

marriage to stop resentment building.

Emily Baxter, a mum to twins,

saw flight costs boom once the

children were past two years old. She

wanted to make sure she could go back

home to the UK at least yearly, and

imaginatively readjusted her budget

to allow for it. “I realised how much

I spent in coffee shops and eating

lunch out,” she says. Trying to keep

the twins active and social came with

a hidden financial commitment. She

calculated that just reducing her coffee

habits for a year gave her enough for a

child’s ticket. “Which is mad, really,”

she says.

Big incentives, like Emily’s, help to

keep resolve high. But weigh carefully

what you can comfortably cut. A spa-

lover who sacrifices every treatment

could become seriously de-motivated,

but that same spa-lover might be

happy to give up her lattes if it means

she can keep her facials and massages.

Richard Bolton, a senior

consultant with The Henley Group,

and a new daddy to a baby girl,

splits his spending into weekday

and weekend budgets. His weekday

spending is usually fairly fixed, while

his weekends are where he loosens

his purse strings on eating out and

entertainment. “You may budget

$2,000 for weekly expenses, like food

and transport, and $3,000 for weekend

expenses, like eating out, kids’

activities or treats, giving you a budget

of $5,000 for the week, or $20,000 for

the month,” he says. Richard takes out

a weekly allowance at the start of the

week, and then withdraws cash for the

weekend separately. “That way, if I’ve

run out by Sunday I know it’s time to

go home,” he says. He advises clients

to get into this habit to monitor money

and incorporate a budget comfortably

and successfully.

Making the grade

Staying home is a great money saver.

Take playdates in turns at home or go

to a local playground. It also pays to

shop local, says mum Eva Wong, since

premium costs on imported products

are high. The market is a great place

to begin. Often fruits and vegetables

from the same depots are sold at both

supermarkets and markets, but are

cheaper at the markets – especially

If you have a budget that you’ve

decided is more than enough, you

avoid feeling guilty saying no when

they ask for more.

October 2013

45